audit working papers are the property of

In order to keep professional ethic it cannot discover to third party without consent of the client unless limited specified situations mentioned in ISA 230 Documentation and required by law the. Audit working papers are used to support the audit work done to assure that the relevant auditing standards performed the audit.

Audit Of Non Current Assets

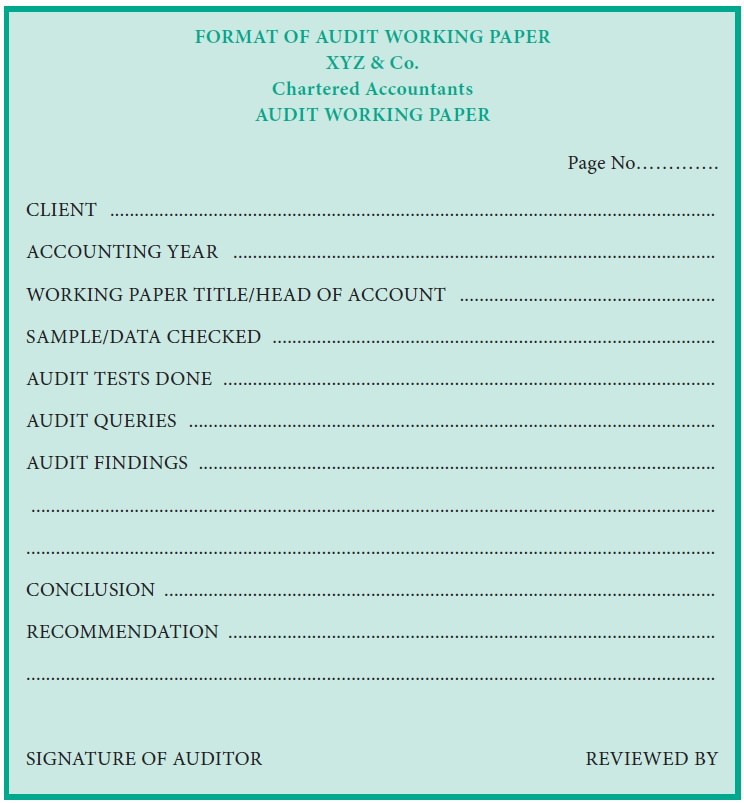

Audit Working Paper Format.

. Ownership of Audit working papers. Evidence of the planning process including audit programs and any changes thereto. If additional evidence is required to document significant findings or issues the original evidence is NOT considered sufficient and appropriate and should be deleted from the working papers d.

The working papers are the matters documented by the auditor. Basically the audit working papers serve the following purposes. Working papers are the property of the auditor and some states have statutes that designate the auditor as the owner of the working papers.

Audit working papers refer to the documents prepared by or use by auditors as part of their works. The Auditor may at his discretion make portions of or extracts from his working papers available to his clients. Audit working papers are the property of the auditor.

To support the financial report. Audit working papers are used to support the audit work done in order to provide the assurance that the audit was performed in accordance with the relevant auditing standards. State the degree to which financial statements follow accounting principles and standards with.

The current file of an auditors working papers is most likely to include a copy of the. The auditor may at his discretion disclose extracts or copies of working papers to the client. Audit working papers are the property of the auditor.

Audit working papers are the documents and evidence that an auditor collects and retains with himself during the audit. Purpose of Audit Working Papers. Audit working papers are sometimes referred to as audit documents.

SBIRT has been defined by SAMHSA as a comprehensive integrated public health. Working papers are the record of various audit procedures performed audit evidence obtained allocation of work between audit team members etc. So they are his property.

Our solutions are written by Chegg experts so. From the above discussion it is clear that working papers are owned by the auditor even though they comprise information that is based on the clients records. Audit documents on client nature of business.

An auditors working papers will generally be least likely to include documentation showing how the. Support as sufficient and appropriate basis in the auditors report. NMCMTFHOSPITALCLINIC NAME 2 The engagement supervisor is reviewing the working papers CV3 2TQ working days of Equally poor records management by internal audit can render the wider Following are the key points of this paper.

The auditors rights of ownership however are subject to ethical limitations relating to the confidential relationship with clients. Prove that the audit has been planned and performed. Audit working papers are the documents which record during the course of audit evidence obtained during financial statements auditing internal management auditing information systems auditing and investigations.

Importance of Auditing Working Papers. Clients schedules were prepared. Here is the example of audit working papers.

Although the client may claim them as a record of his business matters the auditor cannot part with them as his conclusions are based on them and as they provide evidence of the audit work carried out according to the basic principles. They cannot distort them because it can be used as an evidence if there would be. Thus the audit working papers are the property of auditor and not of the client.

The working papers are the property of the Auditor. Which of the following is not a primary purpose of audit working papers. Describe a situation in which a set of audit working papers might be used by third parties to support a charge of gross negligence against the auditors.

In order to keep professional ethic the auditor cannot reveal to third parties without client consent unless limited specified situations exist andor required by law. According to ISA 230 Audit Documentation the auditors objective is to prepare documentation that can. Although audit working papers are property of the auditors they should not be sold distorted or given to third party as it will violate the Code of Ethics of Confidentiality because what is contain in the audit working papers are information about the client.

Access Principles of Auditing Other Assurance Services 21st Edition Chapter 5 Problem 23RQ solution now. Audit working papers are the property of the auditors who may destroy the papers sell them or give them away Criticize this quotation. Audit Working Papers can be defined as the documents that auditors record during the course of the audit whilst they are obtaining evidence regarding the companys financial statements and other relevant transactions.

Those documents include summarizing the clients nature of the business business process flow audit program or procedure documents or information obtained from the client and audit testing documents. Acts as evidence if there is any charge. - a Client - b Accountant - c Auditor - d Registrar of companies - Advance Accounting and Auditing Multiple Choice Question-.

Solved Answer of MCQ Audit working papers are the property of. Working papers are the property of the auditor. Audit working papers are documentation prepared and organized by the auditor to perform a proper audit service.

Evidence of the auditors consideration of the work of internal audit and conclusions reached. They show the audit was. Audit documentation is the property of the client and sufficient and appropriate copies should be retained by the auditor for at least 5 years.

Audit documents of team meeting. Although audit working papers are property of the auditors they should not be sold distorted or given to third party as it will violate the Code of Ethics of Confidentiality because what is contain in the audit working papers are information about the client. The ownership of working papers belongs to the auditor.

According to SAS 41 working papers are the records kept by the auditor of the procedures applied the tests performed the information obtained and the pertinent conclusions reached in the engagement.

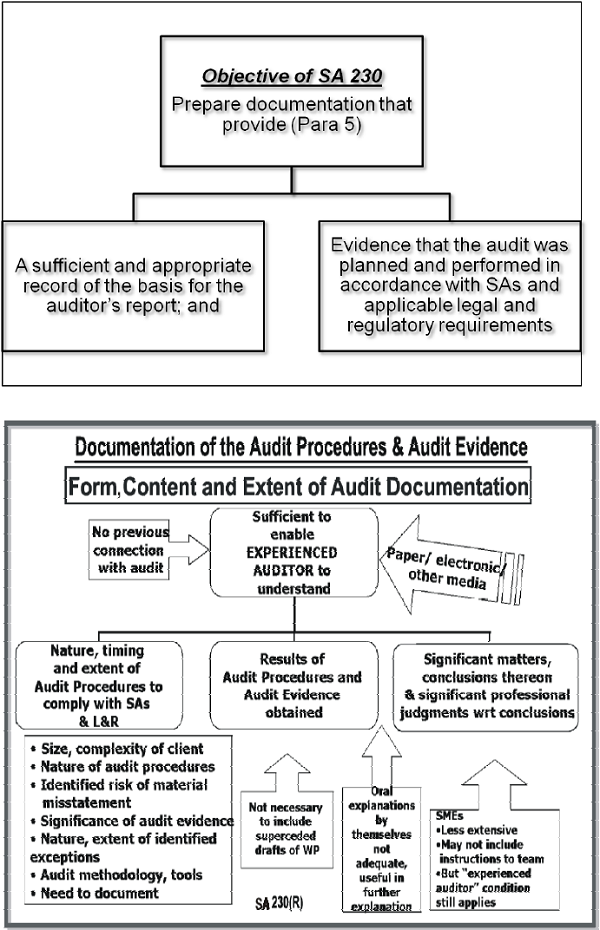

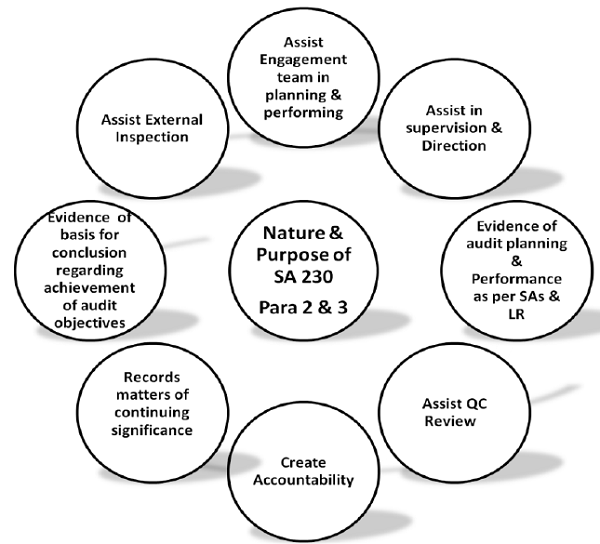

Guide To Standard On Auditing Sa 230 Audit Documentation

Audit Working Papers

Audit Working Papers

Guide To Standard On Auditing Sa 230 Audit Documentation

Audit Working Papers

What Is Audit Working Papers In Auditing Meaning Of Audit Working Papers ह न द म Youtube

Audit Working Papers Meaning Definition Contents Objectives Importance Or Advantages Auditing

Audit Procedures Types Assertions Accountinguide

All About Operational Audits Smartsheet

What Is Audit Working Papers In Auditing Meaning Of Audit Working Papers ह न द म Youtube

Cash Count Sheet Audit Working Papers Balance Sheet Template Bookkeeping Templates Money Template

Internal Auditor Resume Samples Velvet Jobs

Internal Auditor Resume Samples Velvet Jobs

Audit Working Papers

Audit Working Papers

What Are Audit Working Papers Youtube

2

Guide To Standard On Auditing Sa 230 Audit Documentation

Audit Procedures Types Assertions Accountinguide